Over 60% of Canadians Struggle with Financial Stress and Economic Whiplash

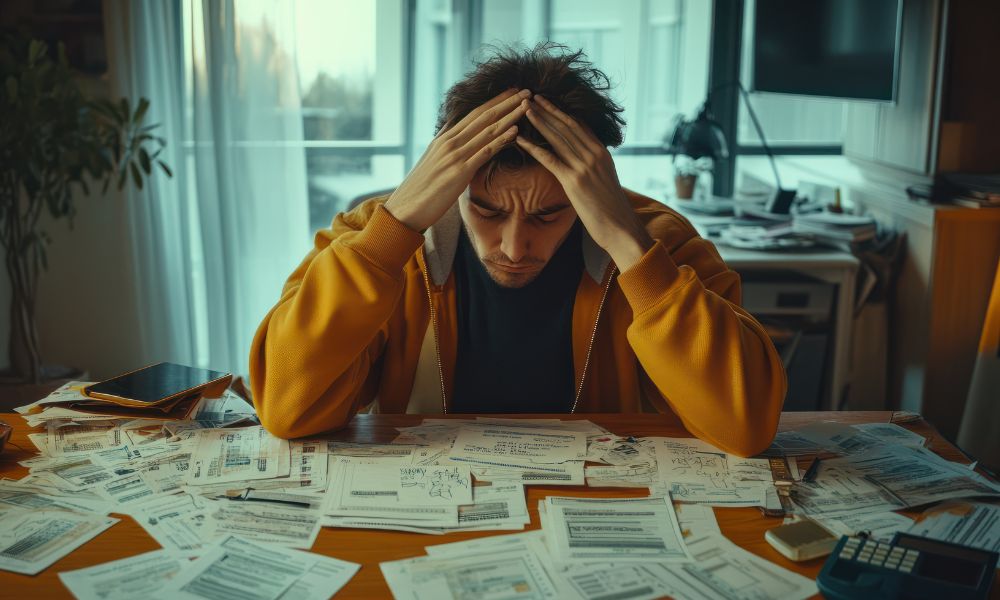

If you feel like you’re on a financial rollercoaster you never bought a ticket for, you are far from alone. A recent study has revealed a stark reality: over 60% of Canadians are grappling with significant financial stress, a condition many are calling “economic whiplash.” This term captures the dizzying effect of rapid economic shifts—from soaring inflation to rising interest rates and housing unaffordability—leaving a majority of the population feeling financially unstable and deeply anxious about the future.

This isn’t just about tightening belts for a month or two. It’s a pervasive sense of insecurity affecting household budgets, long-term plans, and mental well-being. The constant barrage of conflicting economic signals creates a state of chronic stress, making it difficult for families to plan, save, or feel secure. Let’s delve into the key drivers of this national financial strain and explore strategies to navigate these turbulent times.

The Perfect Storm: What’s Causing Canada’s Economic Whiplash?

The financial pressure Canadians feel is not due to a single factor, but a convergence of several powerful economic forces. Understanding these elements is the first step toward managing their impact.

The Relentless Squeeze of Inflation and Interest Rates

For over two years, high inflation has been eroding purchasing power, making everything from groceries to gas more expensive. Just as households adjusted their budgets, the Bank of Canada began a series of aggressive interest rate hikes to cool the economy. This one-two punch is devastating:

- Monthly mortgage payments and variable-rate debt costs have skyrocketed for many homeowners.

- Renters face record-high prices as rental market demand intensifies.

- Everyday essentials consume a larger portion of take-home pay, leaving little for savings or discretionary spending.

This creates a classic whiplash effect: inflation demands more money for daily life, while higher interest rates increase the cost of borrowing and debt, trapping many in a cycle of catch-up.

The Housing Affordability Crisis Deepens

Housing remains at the epicenter of financial stress for Canadians. The dream of homeownership feels increasingly out of reach for younger generations, while current owners face daunting renewal scenarios. The stress extends beyond mortgages:

- Sky-high rental costs prevent many from saving for a down payment.

- Property taxes and maintenance costs continue to rise.

- The psychological weight of housing insecurity affects decisions around family, career, and future planning.

Stagnant Wages and Job Market Uncertainty

While the cost of living climbs, wage growth has largely failed to keep pace for a significant segment of the workforce. This imbalance means that even employed Canadians are falling behind. Coupled with whispers of a potential economic slowdown, job security—a cornerstone of financial stability—feels more fragile, adding another layer of anxiety.

The Human Cost: More Than Just Numbers

The impact of this economic whiplash extends far beyond bank statements. It’s taking a severe toll on the mental and physical health of the nation.

Chronic financial stress is linked to anxiety, depression, sleep disturbances, and strained relationships. The constant worry about making ends meet creates a state of “financial fight-or-flight,” which is exhausting and unsustainable. People are postponing major life decisions, from getting married to having children or retiring, creating a ripple effect that will shape Canadian society for years to come.

Navigating the Turbulence: Practical Steps for Stability

While the macroeconomic forces may feel beyond individual control, there are proactive steps you can take to steady your finances and reduce stress.

1. Conduct a Financial Stress Test

Knowledge is power. Start with a brutally honest audit of your finances.

- Track Every Dollar: For one month, record all income and expenses to identify true spending patterns and potential leaks.

- Review Debt: List all debts with their interest rates. Prioritize paying down high-interest debt first.

- Scrutinize Subscriptions & Recurring Costs: Cancel any services you don’t actively use.

2. Fortify Your Budget for Inflation

Your old budget likely doesn’t work anymore. Create a new, inflation-aware plan.

- Differentiate Needs vs. Wants: Be ruthless in categorizing expenses to free up cash for essentials.

- Plan for Groceries Strategically: Use flyers, loyalty programs, and meal planning to combat food inflation.

- Build a Buffer: Even a small emergency fund of $500-$1,000 can prevent a minor setback from becoming a crisis.

3. Tackle Debt Strategically

High-interest debt is the primary amplifier of financial whiplash.

- Contact creditors to discuss hardship programs or payment plans.

- Explore a debt consolidation loan with a lower interest rate to simplify payments.

- Focus on one debt at a time (using the avalanche or snowball method) to build momentum.

4. Seek Professional Guidance

You don’t have to do this alone. Non-profit credit counseling agencies offer free, confidential advice on budgeting and debt management. For complex situations, a certified financial planner can help create a long-term strategy tailored to your goals.

A Path Forward: Building Resilience in Uncertain Times

The data is clear: financial whiplash is a widespread Canadian experience. Acknowledging this shared reality can reduce the stigma and isolation that often accompanies money stress. By understanding the root causes—the interplay of inflation, interest rates, and housing costs—and taking deliberate, proactive steps to manage your personal finances, you can begin to replace anxiety with a sense of control.

Building financial resilience is not about achieving perfection or keeping up with past expectations. It’s about adapting to a new economic landscape with clarity and purpose. Start with one step, whether it’s tracking your spending, making a budget call, or seeking advice. In a climate of economic whiplash, the most powerful move you can make is to decide to be the author of your own financial story, one stable chapter at a time.